Critical Illness Cover is an insurance policy that pays out a tax-free lump sum if you become critically ill during the policy term.

The levels and bases of taxation and reliefs from taxation can change at any time and are dependent on individual circumstances

What is Critical Illness insurance and how does it work?

Critical illness insurance is a form of insurance that pays out a tax-free lump sum should you become seriously unwell and are diagnosed with a critical illness during the term of your policy.

Critical illness cover pays out a tax-free lump sum if you’re diagnosed with a serious medical condition. The levels and bases of taxation and reliefs from taxation can change at any time and are dependent on individual circumstances. The benefit you receive helps safeguard you and your family against the financial impact of becoming critically ill.

A Critical Illness Insurance payout could be used:

to be put in the bank

to repay the mortgage

to settle debts and bills

to pay for a family holiday

to pay for home conversions

To pay for care or hospital treatment until you feel well enough to return to work

Whatever its purpose, Critical Illness cover provides peace of mind.

Meet Liz

Liz Roland a wife and mother to two children, underwent a bifrontal craniotomy to remove a brain tumour. Liz spent 7 weeks re-learning to swallow, speak, walk and sleep normally again. By her side was her husband who had taken 7 weeks off work to care for her. Luckily, his employers allowed him to remain on full pay and kept his job open for him. Would all employers be so accommodating? What if he was self-employed?

In her own words, she totally underestimated her rehabilitation. Watch this short uplifting clip of how Liz coped and got her health back.

Is critical illness insurance different to life insurance?

Yes, critical illness insurance is different to life insurance. Life Insurance pays out a cash lump sum when you die. Your family benefit from the money paid to them. Critical Illness Insurance pays out a cash lump sum should you suffer a serious illness. You and your family benefit from the money paid out. Find out more about Life insurance.

What conditions count as a ‘critical illness’?

Critical illness conditions are defined as those that are very serious and usually life-threatening. The type of medical conditions which you might not recover from. Medical conditions such as cancer, stroke, heart attack, Parkinson’s disease, Motor Neurone Disease, loss of an arm or a leg for example.

Do you need critical illness cover if you have a mortgage?

To answer whether you need critical illness cover if you have a mortgage, you need to consider the following questions:

How will I pay the mortgage if I were seriously ill and could not work?

Would my savings be enough to pay for adaptations to my home?

Would I be able to afford a full-time carer to look after me?

Would my partner be able to give up work or take extended time off without income to care for me?

Would I be able to pay for transport to hospital/ specialist/ rehabilitation appointments?

Critical illness cover will help to protect your home and keep a roof over the heads of your loved ones. It’s a scary thought that we might get seriously ill and is often ignored because it is a worrying subject. Especially, when 1 in 2 of us will get cancer at some stage in our lives*. Cancer Research UK July 2023. If you are diagnosed with a serious illness from which you may not recover, it can be a very stressful time, especially if you are also worrying about paying bills to keep your family protected. Critical illness is not a legal requirement but if you have dependants or a mortgage, it is a good idea to get critical illness cover.

What isn’t covered by critical illness insurance?

Critical Illness policies vary from insurer to insurer, and their list of conditions and definitions of illnesses also differ. Anything that is not included on an insurer’s condition list is not covered.

What does critical illness insurance cover?

Critical illness covers serious illnesses like cancer, strokes, heart attacks plus many more. Each insurance company will cover a different number of serious illnesses within their policy small print. It is important to choose the most comprehensive plan for you within budget.

All Critical Illness Insurance policies cover three core conditions:

Cancer

Heart attacks

Strokes

Critical Illness policies vary from insurer to insurer, and their overall list of conditions and definitions of illnesses also differ.

More comprehensive plans will also cover conditions such as early stage prostate cancer, angioplasty, lower grades of breast cancer, loss of hearing and sight, total permanent disability, multiple sclerosis, Alzheimer’s disease, and Motor Neurone Disease.

We can advise you on the most comprehensive policies available in the marketplace.

A good critical illness plan may cover:

Alzheimer’s disease – resulting in permanent symptoms

Aorta graft surgery – for disease or following traumatic injury

Aplastic anaemia – of specified severity

Bacterial meningitis – resulting in permanent symptoms

Benign brain tumour – resulting in permanent symptoms

Blindness – permanent and irreversible

Cancer – including advanced skin cancer

Cardiac arrest – with insertion of a defibrillator

Cardiomyopathy – of specified severity

Chronic rheumatoid arthritis

Coma – resulting in permanent symptoms

Coronary artery by-pass grafts – with surgery

Creutzfeldt-Jakob disease – resulting in permanent symptoms

Deafness – permanent and irreversible

Dementia – resulting in permanent symptoms

Encephalitis – resulting in permanent symptoms

Heart attack – of specified severity

Heart valve replacement or repair – with surgery

HIV infection – from a blood transfusion, a physical assault or at work

Kidney failure – requiring dialysis

Liver failure – end stage

Loss of hands or feet – permanent physical severance

Loss of independence – of specified severity

Loss of speech – permanent and irreversible

Lung disease – of specified severity

Major organ transplant

Mastectomy for ductal carcinoma in situ (DCIS)

Motor Neurone Disease – resulting in permanent symptoms

Multiple sclerosis (MS) – with persisting symptoms

Multiple system atrophy – resulting in permanent symptoms

Open heart surgery – with surgery to divide the breastbone

Paralysis of limbs – total and irreversible

Parkinson’s disease – resulting in permanent symptoms

Pre-senile dementia – resulting in permanent symptoms

Progressive supranuclear palsy – resulting in permanent symptoms

Pulmonary artery replacement – with surgery to divide the breastbone

Respiratory failure – severe lung disease – of specified severity

Stroke – of specified severity

Systemic lupus erythematosus (SLE) – of specified severity

Third-degree burns – covering 20% of the body’s surface area or 20% of the face’s surface area

Traumatic head injury – resulting in permanent symptoms

Type 1 insulin-dependent diabetes mellitus – of specified severity, diagnosed after the age of 40

Ulcerative colitis – treated with total colectomy

There can be vast differences between insurers’ policy terms (small print), so it pays to take some expert advice. Our knowledgeable team are happy to explain which policies offer the most comprehensive Critical Illness cover at the most competitive prices.

What are the benefits of critical illness insurance?

The benefits of critical illness insurance are many and varied. It can provide peace of mind if you don’t have substantial savings.

It isn’t just the money that can pay for your mortgage, loan repayments and household bills. The breathing space that the money provides can bring great relief if you are recuperating. It allows loved ones time off work without the added worry about their lost income. So that they can spend time with you, in what could be your last few months.

A major aspect that is often overlooked when a person is critically ill is the length of time and help necessary to recover.

This can include physiotherapy, chemotherapy, counselling, or adaptations to your household so that you can remain at home.

Do I need critical illness cover?

We are approached by many clients asking us if they need critical illness cover. We ask them if they have:

Substantial savings that won’t run out and if they have someone to rely on indefinitely for your long-term care?

Can they guarantee that they will never get a critical illness or suffer a life-changing accident?

Would you be able to survive on the Government’s sick pay of up to £109.40 a week (up to 28 weeks)? Find out more from the Government website. If the answer is ‘no’ to any of the above, Critical illness protection should be a consideration for both you and your family. Why not take a look at your personal risk profile on the Future Proof risk reality calculator?

Peace of mind if you don’t have substantial savings: If you don’t have a savings pot, critical illness cover can be reassuring to help pay for the bills.

Loans to pay off: If you fall critically ill and can’t work, the pay-out can settle any outstanding payments like your mortgage or loans.

Your children can be included in your policy so that the whole family is protected comprehensively.

If there are dependants: Critical illness cover can give you peace of mind if you have children or other family members that rely on you financially.

Rehabilitation: A payout can pay for your rehabilitation such as physiotherapy or counselling. It can pay for household adaptations or modified transport so you can live more independently again.

Cons

Not all illnesses are covered: Future Proof will find the most comprehensive policies available. We can clarify exactly what illnesses are covered by your insurance provider. Critical illness should not be confused with income protection. Many minor but still debilitating illnesses can prevent you from being able to work that are not listed under a critical illness policy. This is why an income protection policy should also be considered.

Critical illness cover will cost more than life insurance, as the risk of becoming critically ill is greater than the risk of passing away. Premiums rise as you get older, and as the likelihood of your making a claim rises, it is better to lock in lower rates when you are younger.

You already have an employee benefits package: A package that will pay out if you fall seriously ill during your service. This is very useful, but what if you were to leave employment? Premiums rise as you get older, and critical illness premiums may be out of your budget range if you apply at an older age once employment ends.

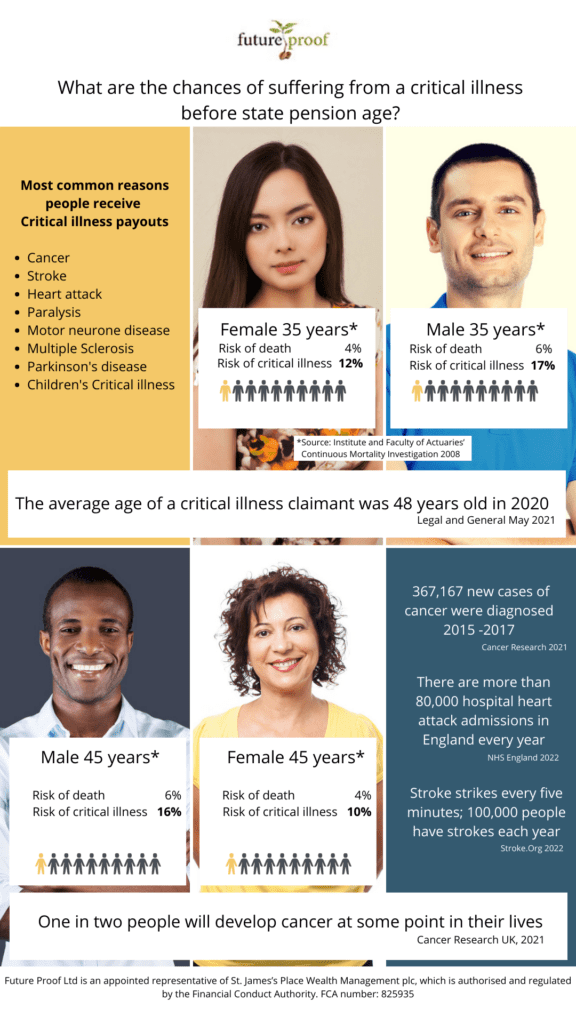

What are the risks of me getting a critical illness?

The risk of getting a critical illness or becoming too ill to work for a few months is highlighted below.

How much critical illness cover do I need?

To establish how much critical illness cover you need, you will need to do a few calculations.

How much money would you need to cover your outgoings, if you were to fall seriously ill? Your Future Proof adviser can help you with this.

Outgoings you’ll need to consider include:

· Your mortgage or rent payments: Work out how much you have left to pay on your mortgage, or how much your rent payments would total over time

· Household bills: You will need to include the costs of your regular bills like gas and electricity, council tax, car insurance and water

Debts you’re paying off over time: These might include any loans or credit card payments you have yet to clear

· In the event that you are unable to work due to illness, you’ll need to include how much money you would need to provide for your children and family. Childcare is expensive, is it necessary to include school fees in childcare costs?

· Medical expenses: Having to adapt your home to meet your needs should you fall seriously ill, or travel to the hospital for medical treatment

· Would a Partner need to take time off work to care for the other whilst they recuperate? For example, seven weeks off work – how much would be lost in salary?

Critical illness cover comparison

Comparison websites are available for everyone to use when it comes to comparing critical illness cover. However, their use depends on you knowing precisely what you are looking for, which can be tricky when it comes to critical illness insurance.

There are many different factors and variances between policies and insurers. To find out the most comprehensive policies will involve you reading the small print of each policy. Here are a few points that highlight the differences between sourcing cover through an adviser and a comparison website.

Adviser

Comparison site

Is qualified to give advice about a product

Will not give you tailored advice

Provides a one-to-one relationship from start to finish

Other than providing a list of insurers and premiums cannot advise you if you have a query, need an explanation of small print or help with a future claim

Has a broad product and insurer knowledge with minimal gaps

A comparison site relies on your research and your choice

MUST ensure the policy is right for you

Comparison sites have no such obligation. The onus of making the right choice of protection for your family is on you

Will understand the policy wordings and can explain in simple terms

You must read and understand the wording yourself

Will have buying power and close relationships with insurers

A comparison site will leave the post-application discussion to you

Am I eligible for critical illness insurance?

You will be eligible for critical illness insurance as long as you are aged between 18 and 70 years, you are a UK resident and you have a UK bank account.

What information would I need to give to get a quote?

To give the insurers a good idea of the risk they will be accepting our advisers will ask you for the following personal information:

Your age

Whether you smoke

Whether you have used any form of recreational drugs in the last 5 to 10 years

How many units of alcohol do you drink in a week?

Your height and weight ie Body Mass Index

Is there a family history of serious illness before the age of 65 years (parents and siblings)?

Whether you have any pre-existing medical conditions such as diabetes, high blood pressure or Arthritis

Do you have a high-risk occupation? Eg working at heights, in dangerous countries, at sea?

Do you take part in any hazardous pursuits? Eg diving, rock climbing, sailing, motor racing?

We are advisers, not salespeople. You and your family come first and are at the heart of any advice that we provide. We are also specialists that regularly help people with challenging health situations, hobbies or risky professions. We are here to help you make informed decisions.

How much does critical illness cost?

The risk of people getting a serious illness or being affected by an accident is higher than the risk of them dying. Owing to this, the cost of critical illness cover will be higher than the cost of life insurance.* These probabilities are based on the rates of a critical illness occurring, published by the Institute and Faculty of Actuaries’ Continuous Mortality Investigation (’08’ series accelerated critical illness morbidity tables).

The following factors affect the premium you are offered:

Generally, the older you are, the more you should expect to pay for a policy. That’s because you’re considered more of a risk to an insurance provider as you get older. You’re more likely you will be affected by a critical illness, during your ‘policy term’ – that is, while the policy is running. There can be cost benefits to buying critical insurance when you’re younger.

If you get insurance when you’re younger, you’ll pay lower premiums-and they will stay the same for the duration of your policy.

It can be challenging to obtain critical insurance when you are significantly underweight, overweight or obese. It can often result in the premium you were originally quoted being increased (loaded) once the application has been assessed. In some cases, the application can be declined. Their process may include them writing to the GP for a medical report or asking you to attend a short medical assessment (which the insurer pays for).

The purpose of a loading is to reflect the additional risk the insurer assesses they may be taking on (compared to someone with a normal BMI / no medical declarations).

To assess how much critical illness cover you need, your Adviser will ask you the following questions:

Mortgage – How much is outstanding? What is the remaining term of the mortgage?

Rent – How much rent do you pay per month? Also, consider how much your rent may increase in the future

Debts – What is the total amount owed and over what term?

Outgoings – regular monthly bills such as travel costs, utility bills, council tax, school fees, maintenance payments perhaps?

Family – How many children/dependents do you have? How old are they? And how long do you feel they will be dependent upon your income/care?

As a starting point for the amount of critical cover, take your gross annual earnings and double them. See how much the monthly premium comes to and then tweak from there to fit your budget. Our Advisers will help you find the balance between cost and the most comprehensive policy for you and your family.

There’s not much you can do about your family genetics. Having a family with a medical history of stroke, cancer, or other serious medical conditions may predispose you to these ailments. This may contribute to higher critical illness premiums. Typically, insurance companies are interested in any conditions that affected your parents or siblings, particularly if they contributed to premature death. There are insurers who place more emphasis on your family’s health than others. It is likely that it will affect your premium and may be excluded from the policy conditions.

Your lifestyle could affect the premium that you will pay. Is your favourite pastime racing cars, scuba diving or climbing treacherous mountains? If so, you’ll probably have to pay higher premiums for critical insurance. Insurers worry about life-changing accidents when you take part in high-risk activities.

Smoking puts you at a higher risk for all sorts of health ailments, cancer being one of them. Smokers pay more than non-smokers for comparable coverage.

Alcohol consumption

Drug taking – including non prescription drug use.

Asthma

Cancer

Arthritis

Obesity

Diabetes

Cholesterol

Mental health conditions

Heart disease / high blood pressure

Insurers will need to know if you’ve had a health issue in the past – whether that is recently, or at any point in your life.If the condition is severe or one that may deteriorate with age, it may not be covered under a critical illness policy.

To assess how long your life policy is best to run for, your Adviser will ask you:

How long is the term of your mortgage?

What is your expected retirement date?

How many years do you think your children will be dependent on you?

Do you have any outstanding loans – over what term are they?

The answers to these will help determine the length of the critical illness insurance policy. What we want to avoid is the term ending too early whilst the need for critical illness cover is still there. Re-applying for insurance at an older age will mean you paying a higher premium over an extended term.

Some occupations are more dangerous than others eg working at heights, diving, overseas travel, working in the armed forces. If you work in a job that’s high-risk, it may mean that you will pay higher critical illness premiums.

Examples of monthly premiums

This table gives you an approximate idea of monthly premiums for stand-alone critical illness cover.

Please note that any premiums mentioned are indicative only and based on this specific case study/ example, which is shown for information purposes only. Premiums shown are an average of the 5 cheapest insurers. Your own circumstances will determine whether the amount payable is more or less than the figure quoted.

Quotes provided July 2023.

Quotes based on male, non-smoker, to age 65.

Age of client in years

Sum assured in £s

Term

Type of cover

Monthly premiums in £s

30

£30k

To age 65

Level critical illness only

£10.90

30

£100k

To age 65

Level critical illness only

£29.89

40

£30k

To age 65

Level critical illness only

£16.14

40

£100k

To age 65

Level critical illness only

£47.54

50

£30k

To age 65

Level critical illness only

£27.56

50

£100k

To age 65

Level critical illness only

£85.85

Are some types of critical illness cover better than others?

This can become a minefield when deciding which company offers the most comprehensive policy. It’s not simply about the number of conditions covered –it’s also about the small print, this explains the degree of severity of the conditions accepted at the claim stage.

It is important to seek expert advice to ensure you have the most comprehensive policy available.

How should I compare critical illness policy offers?

It would be impossible for an individual to adequately compare all critical illness policy offers.

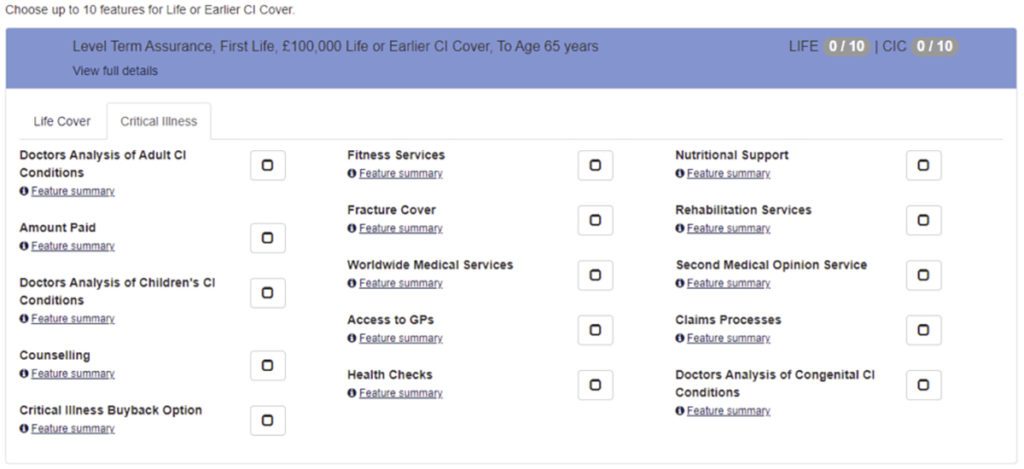

Future Proof use software systems called CI Expert and Solution builder to assist us in this task. This helps our Advisers find the most comprehensive policies and strike a balance with premiums. These technologies show us lists of considerations to choose from, then filter the marketplace offering by showing us appropriate insurers and their policies. Listing the most basic to the most comprehensive and their premiums.

An adviser, will take the findings and apply them to your personal situation.

If you have children – which insurer has good children’s cover included in the premium?

If you play rugby – good fracture cover would be a wise consideration.

If you have family history concerns over cancer for example – the insurer with the widest definition of cancer would be suggested.

Generically, if you have no such specific concerns, our Advisers will look at your budget and find the most comprehensive policy that strikes a balance with this.

The image below is a screenprint of the software our advisers use to help them find the most appropriate cover for your circumstances.

What factors can affect the cost of critical illness cover

The following factors can affect the cost of critical illness cover:

Your age

Lifestyle – do you smoke/ stay within recommended alcohol drinking guidelines?

Your weight – are you over or underweight?

Your medical history – any medical conditions which might contribute to a future claim?

Your family medical history – any serious conditions suffered by your parents? Grandparents? Siblings?

Do you have a risky occupation? Work at heights, dive?

Any high-risk hobbies? Motor racing, rock climbing

If you are older and tick any of the factors above, your premium may be higher than a young, fit healthy person who has a low-risk job and sedate hobbies.

These factors will be assessed at the application stage. At Future Proof, we ring insurers ahead of your application to gauge their reaction. We only apply to those insurers that are most sympathetic to whichever factors affect you. Saving you time and money.

Yes, you can get critical illness cover without life insurance, it is sometimes referred to as stand-alone critical illness.

In more detail, stand-alone critical illness is a critical illness policy which has no life cover element. In that, it purely protects against the financial impact of becoming critically ill.

Cheapest critical illness insurance

The cheapest critical illness insurance is most often not the most cheerful. Plans vary greatly in the number, severity and type of conditions covered. All critical illness policies are not the same. By not comparing the policy conditions with others and just going by price, you would be doing yourself a huge disservice. Our Advisers know the best plans and the most accommodating of insurers. Let them do the research for you at no-obligation.

Critical illness insurance benefits

Each critical illness insurance plan will have its own additional benefits. Here are the main ones:

Hospitalisation cover is included in some of the more comprehensive critical illness insurance policies. A pay-out will be given if you’re admitted to hospital with a severe physical injury resulting from an accident, and you may need to stay there for a number of consecutive days eg 28. If this cover is included within your policy, you could receive up to 20% of the sum assured, or £50,000, whichever is the lower depending on the insurer.

Many insurers’ Critical Illness Insurance policies also provide cover for ‘less severe’ conditions, which are usually described as Partial Payments. Diagnosis of one of these conditions may result in up to 25%- 35% of the sum assured being paid.

Even if a successful claim is made for a partial pay-out, the policy can usually continue without a reduction in the sum you are insured for.

When you take out a critical illness insurance policy, it’s vital you keep up with the monthly payments. A missed payment could mean your policy is cancelled. But what if you can’t pay because you’re ill or seriously injured and unable to work?

This is where a waiver of premium comes in. If you can not pay, this add on will pay your critical illness insurance premium for you. It is an insurance policy that covers your insurance premiums.

Waiver of premium can be added to your critical illness policy for a nominal price.

It is only available if you are employed, and usually only until you reach 65.

This kind of cover is available as part of a regular (adult’s) critical illness cover. Most insurers will include it in your policy at no extra charge. Some charge a nominal sum to include children’s cover.

Many insurers offer a range of additional benefits and support services alongside their core cover, designed to provide clients with either additional help or a further financial safety net if required. One such benefit offered by a few insurers is fracture cover.

It is easy to assume that fracture cover is only really necessary for those who participate in certain sports or work in manual trades. Fractures, however, can have serious financial implications for many clients, especially if they are forced to take time off work to recover.

Where fracture cover is available it will be either free or included at an additional cost. Fracture cover is provided in addition to the main listed conditions. Meaning, there is no requirement that you have to claim on a main listed condition to be paid fracture benefit. Likewise a claim for fracture cover will not impact the main policy in any way.

Total Permanent disability is an additonal benefit that pays out an agreed sum of money if you have an illness or injury that means you’re permanently incapacitated.

Insurers define total permanent disability by how it impacts your work and daily life. These are explained below.

Own Occupation Total Permanent Disability

TPD can be offered on an ‘own occupation’ basis for low risk workers eg office workers. This means that the policy could payout if you are totally and permanently unable to work in your own job due to sickness or injury. This is the most comprehensive definition as you would be covered if you could no longer do your own job.

Suited Occupation Total Permanent Disability

This means that the policy could payout if you are totally and permanently unable to work due to sickness or injury in an occupation for which you are suited given your skills and experience.

Any Occupation Total Permanent Disability

This means that the policy could payout if you are totally and permanently unable to work due to sickness or injury in any occupation whatsoever.

OK, so the insurer has paid out your lump sum. Have you thought about recovery and rehabilitation needs? Insurers offer benefits such as Helping Hand and dedicated nurses. Additional benefits such as, private GP services, mental health support, nutritional and fitness advice are also available. Each insurer will have its own additional benefits which can be found in detail HERE.

Children’s critical illness cover

No one likes to think about the possibility of their child becoming critically ill. Whilst children’s critical illness cover is not available to buy as a separate policy, this kind of cover is available as part of a regular (adult’s) critical illness policy. Most insurers will include it in your policy at no extra charge. Some charge a nominal sum to include children’s cover. This may appeal if you don’t have children and aren’t planning on having any in the future ( but even if you did, you can add in the children’s cover at a later date).

If the worst happened and your child became critically ill, you or your partner would need to take time off work to look after them. How would you cover your income and pay for your household bills? This is where children’s critical illness cover can help.

In a typical critical illness policy, children will be covered for the same core illnesses and conditions as adults. Some policies may also include some child-specific illnesses, including:

Type 1 diabetes

Cerebral palsy

Cystic fibrosis

Down’s syndrome

To make a children’s critical illness claim, your child’s illness or condition will always need to meet the insurer’s definition, stated in your policy. The definition usually includes a required severity level or symptoms, just like a regular adult’s policy.

As children’s cover is included as an additional benefit, it will only pay out a proportion of your insured amount.

The good thing about children’s critical illness cover is that if a children’s claim is made, the main policy will be unaffected. Your policy remains in place, and you can still claim the full amount later if you yourself are diagnosed with a critical illness.

The age of children covered within an adult policy will vary between insurers. We can advise on the most suitable insurers according to your family situation. Typically, any children (biological, legally adopted, or step) are covered up to their 22nd birthday. Although some insures provide cover only up until their 18th birthday and some beyond age 22.

There isn’t usually a limit to the number of children covered.

The difference between protection products

Life insurance cover does not automatically cover critical illness. Critical illness is an optional extra which incurs an additional cost. Life insurance does however include something called terminal illness benefit which is fundamentally different to critical illness and should not be confused with it.

Terminal illness is an illness from which you will not recover, and are likely to die within a period of 12 months. Most life insurance policies include Terminal Illness cover. This means that they will pay a claim to the policyholder if they are diagnosed with a condition that they are very likely to die from in the next 12 months. This allows the policyholder to take care of their personal affairs before they pass away.

Critical Illness is an illness from which you could well recover and even return to normal life afterwards. As a result of advances in medicine and medical care, many critically ill patients now survive illnesses that were previously fatal.

Income Protection pays out a monthly replacement income if you cannot work due to illness or injury. The benefit can be used to help pay monthly bills, replace income and/or cover mortgage payments. It pays out until you are able to return back to work or until you retire. Some budget-friendly policies pay out for a set period of time like 1,2 or 5 years.

Critical Illness Insurance pays out a lump sum if you become critically ill (and the condition is covered by your policy). The lump sum payout could be used to repay the mortgage, settle debts or pay for medical expenses. All Critical Illness policies cover three core conditions: cancer, heart attacks and strokes. The critical illness conditions that you will be covered for will vary from Insurer to insurer.

When it comes to planning for your future, it is easy to believe that illness or accident won’t happen to you. Many people feel fit and healthy and believe that it is a safe bet to choose Critical Illness cover over Income protection and save themselves from paying another monthly premium.

But, did you know that the following list of illnesses and conditions is not covered by Critical illness insurance? And yet, listed are some of the most common illnesses that create debilitating pain or mental anguish. Which, can go on for weeks before symptoms ease or you get better enough to return back to work.

Shingles

Fibromyalgia

Endometriosis

Broken bones

Frozen shoulder

Slipped disc

Mild depression/ anxiety

Arthritis

Kidney stones

Gall stones

Sciatica

Stomach ulcers

Acute pancreatitis

Pregnancy related complications

Critical illness and income protection complement each other and are very different.

Here are some frequently asked questions by our clients:

When considering taking out a critical illness insurance policy have a think about your family’s needs.

What do you need the critical illness insurance to cover?

Lost income from not working?

Do you have a debt that needs paying?

Do you have anyone dependent on you or your income?

How many years until you pay off your mortgage?

These answers will guide you to how much critical illness cover you need.

Then consider, can you afford the premiums in your monthly budget?

Does your employer offer critical illness cover? What if you were to leave their employment?

Our advisers can talk you through everything that you need to know, so that you can make the most informed decisions.

A critical illness policy can last until your 85th birthday. Or, with some insurers your 90th birthday although these plans are more expensive.

However, the length of the policy can be chosen to coincide with the age when you choose to retire. Or, when you expect to pay off your mortgage.

Joint critical illness cover is available, where one single policy exists for the both of you and only pays out once. It is important to note that if a claim is made, it will leave the other person without cover. If they are older and still require cover, the cost of premiums may then be prohibitive. Whereas, if each person takes out their own policy, making a claim will have no impact on the other person and they will still have cover.

Obtaining critical illness insurance that includes a pre-existing medical condition, is very much dependent on the type of medical condition and its severity.

Some insurers will consider pre-existing medical conditions.

They may offer full cover with a higher premium which is called a rating or loading. Your higher premiums cover the additional risk that your medical condition poses to them if you make a claim.

Whatever the pre-existing condition, part of our process is to pick up the phone and call insurers to ask for their opinion before you apply. Future Proof work with not only the well known protection insurers, but also specialist insurers who do not deal directly with the general public. Based on this outcome we then help you apply to the most sympathetic and get you the cover you need.

To assess your current health and pre-existing condition, Insurers may request a medical report from your GP or a private medical examination ( which they will pay for).

Once your policy is in place, you can adjust the level of cover. It is possible to write to your insurer and reduce the amount you have insured if necessary.

If you are looking to increase the amount insured within the same policy, it would have to be due to one of the following reasons:

Your mortgage has increased

You have welcomed a new child to the family

You have married or entered into a civil partnership

Your salary has increased and your career progressed

You will be able to increase the amount insured without a new application, or medical examination if you were accepted at standard rates. ( ie your policy did not have its premiums increased because of a pre-existing medical condition for example)

This is called the Guaranteed insurability option (GIO). Every insurer has different limits to how much a policy can be increased by ( including an age limit) . In addition, a declaration of health will also need to be signed by the policyholder. This is to confirm that their health has not changed since the previous application.

If however, you need to increase the sum insured outside of your insurers GIO limits then this will require a new application.

Typically, critical illness covers long-term, serious medical conditions. The Association of British Insurers (ABI) is a trade association made up of insurance companies in the United Kingdom. In 2014, the ABI wrote a guide to minimum standards for Critical Illness Cover. This has subsequently been updated in 2019.

The conditions – cancer, heart attack and stroke all remain at the core of each critical illness policy.

Today, insurers vary in the number of conditions covered in their policy’s.The definitions of how serious an illness has to be for a claim to be paid also differ. It is important to get expert advice on the best policy available to you.

Where can I obtain a critical illness policy?

Many life insurance companies, also sell critical illness cover. Whilst comparison sites may seem like an easy route to obtain a quote, the power of a critical illness policy lies in whether a claim will be paid when you need it to.

Advisers like Future Proof will find the most comprehensive policy for you with an insurer that has high payout rates. All insurers offer different levels of cover, which can only be broken down by reading the small print. We can do this for you. Our service is no obligation and you won’t pay us directly. We get paid by the insurer if you take up a policy with them.

Critical illness claims and payouts

Critical illness insurance payouts

Insurance companies want to payout, as strange as this may sound. In 2022, Critical illness insurance payouts totalled over £1.2 billion, according to data from an Association of British Insurers (ABI) news release in June 2022. No one would pay for critical illness insurance if it didn’t pay out. All the insurers compete with each other for your custom, so it is in their interests to have high claims figures. High claim rates tempt customers to place their hard-earned money with them in the form of premiums.

With critical illness insurance not being a legal requirement (unlike motor insurance), it doesn’t make good business sense for them to be seen not paying out.

How many critical illness insurance claims are paid out in the UK?

According to the Association of British Insurers (ABI – is a trade association made up of insurance companies in the United Kingdom), 92% of critical illness insurance claims were paid out in 2022.

According to data provided in an ABI news release in June 2023.

Meet Pete and his family

Having held an insurance policy for four years, he was surprised at having to make a claim so early in the term. Pete is 39 years old.

Each year insurers publish their most common critical illness insurance claims. Whilst these vary between insurers, broadly the most common conditions at the claim stage are:

1 Cancer

2 Heart-related claims

3 Stroke

4 Childrens critical illness claims

5 Multiple sclerosis

The Association of British insurers 2018 tells us that 80% of claims fall into the first three conditions.

Where partial payments and children’s claims are made you will be able to claim on your critical illness policy more than once.

Many insurers provide cover for ‘less severe’ conditions. These are usually described as Partial Payments. Diagnosis of one of these conditions may result in up to 25% of the sum assured being paid. If you have been given a partial claim, you will still be able to make another claim for a different condition.

If a children’s claim is made, the main policy will be unaffected. Your policy remains in place, and you can still claim the full amount later if you yourself are diagnosed with a critical illness.

If you have claimed and the full amount of the sum insured is paid out, your policy will end and you will not be able to make another claim.

Much like car insurance, you do not get your money back if you never make a claim. There is no investment value in the policies that we recommend.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.